90% of car buyers ask this very same question because they have failed to do their homework before ever setting foot on a dealership lot. Before you even think about walking into any car dealer, be it a manufacturing dealership or even a fly-by-night used car lot, you need to do research and homework first. There are 3 things you need to answer before you decide on that decked out Expedition or Lexus FX470:

1. Am I going to buy new or used?

2. How much car can I afford?

3. How am I going to pay for it?

New or Used

In most cases, the answer to this question will be used. Motor vehicles are a product that will depreciate over time, just like any other product. When you finance $45,000 on a brand new car, title it and drive it off the showroom floor, it is now considered a used car and subject to deprecation. Depending on the make and model, that deprecation schedule could be anywhere between 10 – 15% -- just for driving it off the dealer lot! Remember that $45,000 you just financed, also included taxes, title, license, dealer added profit incentives and maybe an extended warranty. So in reality, the basic cost for the vehicle was close to $37,000.

Assuming this particular vehicle has an initial deprecation of 12.5%, that puts the car you just bought, now consider a used car, valued at $32,375. Three weeks down the road, before you have made your first payment to the bank, you are involved in a traffic accident when some clown runs the red light and T-bones you at an intersection. You walk away with minor injuries because of all the safety equipment on this car, but the insurance company totals the car out. All the insurance company is going to pay you is the value of the vehicle at the time -- $32,375. Which means you still have to cough up $7,625 back to the bank. This is the best illustration on making the decision to buy a used car instead of a new car.

What about a lease you ask? For most folks, you’ll be throwing money down the drain. Yes, the payment schedule does look nice, especially when your looking at close to a $500 car payment when buying a used car, but in the long run you will never get ahead. Most leases run for either 24 or 36 month with a restriction of 10,000 miles per year. Anything over that is going to cost you $0.25 per mile. That can add up if you put a lot of miles on a car. Then there is the residual cost at the end of the lease and if the value of the car does not make at least the residual, then you are out that money also.

The only folks that will make out on a lease are those business owners who can write their car off as a primary transportation mode for their business when it comes time to do their business taxes.

Now that we have established that you really need to consider a used car, just how old of a used car can you look for. You best value is a current model year such as a lease return or a Program Car. Normally these current model years will have anywhere between a few hundred miles to several thousand. Normal “wear and tear” on a car is considered between 1000 and 1250 miles per month. If you are looking at a current model year with 25,000 miles, steer clear. Remember, these vehicles still have the remainder of the manufactures bumper-to-bumper manufacture warranty and they usually run out at 36,000 miles or 60,000 miles, depending on the manufacture.

On the other end of the used spectrum, do not look at anything older than 3 years from the current model year. These vehicles that are reaching the 3-year point may have some of the manufactures warranty left. My personal preference is to look for a car that is 2 years old with less than 25,000 miles. In the 17 years that I have been purchasing vehicles from the local Ford and Lincoln dealership, I have purchased 1 current model year with 10,000 miles and this past week, our 5th vehicle, all of which were 2 years old.

How Much Car Can I Afford?

It is unfortunate that only about 15% of the car buying public will actually ask themselves this questions BEFORE they start looking for a car. This is your #1 homework item when you start the search for a new car or truck. There are a lot of factors that you will have to consider, although, ultimately, it will come down to how much you are willing to put out each month for a car payment. Whatever you do, don’t walk into a dealer and tell a sales representative that you are looking for a set of wheels and you only got about $400 per month to spend. They will put you into a vehicle!! It will be the cheapest piece of crap they can find while maximizing their profit and commission.

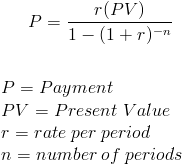

For a good portion of our society, determining how much we can afford is going to be payment driven, unless you have the resources to pay cash. So, you have reviewed your financial situation and you have calculated that you can afford at maximum monthly payment of $475. The formula for computing a loan payment is shown below:

The present value (PV) is the amount of money you are going to finance. (r) is the interest rate divide by 1200, and (n) is the number of periods in months. Run those number into your calculator and it will spit out a payment. If you want to figure out just how much you can finance with a known payment, then you will have to solve the equation for PV which should be quite easy for anyone that has been through a first year Algebra class. It will look something like this:

PV = P *((1 – (1 + r)-n) / r)

Let’s assume that you have a maximum of $475 you want to shell out. Your financial institution will give you a loan for 48 months at 2.9%. To get the rate number for the formula, you have to convert that into a month portion of the annual percentage rate. First divide it by 12 to get the monthly rate, then divide it again by 100 to get the actual rate number that represent the percentage. In this case that number works out to be 0.00242. Plugging these number into your calculator will give you a PV, present value, or the total amount financed of $21,501.07. If you are willing to go to 60 months, then that value will increase to $26,497.73.

It pays to shop around to find the best interest rate possible. Normally a credit union will be your best bet as opposed to a bank, or god forbid, dealer financing. My best deal was 1.49% for 36 months at my Credit Union. During my latest negation with the dealer, the finance guy offered to beat my rate, a feat I knew he could not do, but I pacified him and told him I already had the deal sealed at my CU, but if he could beat 1.49% and prove it, I’d buy him a case of beer. But if he was unsuccessful, then he owed me a case of brew. When I drove the car home, there was a case of Goose Island with a note that simply said 2.66%!!

You have elected to go with a 60-month financing schedule so the bottom line, or the amount you are going to finance is roughly $26,500. If you have additional cash as a down payment and a trade-in, then you have to add that to scheme. You have $5,000 cash you are going to use as a down payment and your trade-in is worth $5,000. So, your bottom-line, out the door cost will be $36,500.

Now you have to work backwards to get to the actual price of the vehicle.

Negotiated price 30,010

Sales tax (6.8%) 2,041

Total 32,051

License fee and tax 550

Documentation fee 399

Dealer options 500

Extended warranty 3,000

Bottom line 36,500

Once you get to the Total Line, then figuring the tax is quite simple. Take the tax rate, 6.8% in this case and divide it by 100 then add 1. We get 1.068. Divide the total value, 32051 by 1.068 and that will give you the negotiated price. The difference between this number and the total will be the amount of sale tax you will have to pay. The License fee and tax will be the cost to register the car plus any Personal property tax or use tax that is levied by your state/county.

Documentation fees! This is really a crock of crap that I like to call Dealer Added Profit (DAP), and unfortunately, there is not much you can do about it. The dealer is going to change you this fee to do all of the leg work to transfer the title and license the car. If the dealers were force by the state to properly do the title work when they take these used cars in on trade or from the wholesaler, then they should be able to give you the properly notarized title and you could do it yourself for $25 - $50. But, the dealers have worked themselves an exception to state law that required you to title a vehicle in less than 30 days, so they can charge you this fee.

Dealer options are anything else that you might negotiate in the deal. Many dealers have something called a Maintenance for Life plan that will let you bring the car in, every 3000 – 5000 miles and get the fluids checked and changed along with filters, and rotate the tires. They will also do an inspection of the vehicle to find anything else that might be in need of repair. If you price this service at many of the Oil change places, you will find that these deals offered by the dealer are a great deal and I’d recommend you consider it as a safety net.

Last, but by no means least, is the extended warranty. Today’s cars are computers on wheels. I stared working on cars when I was a teen back in the late 60’s and early 70’s. Working on a car back then was simple assuming you had a set of hand tools. The design of today’s cars is not even close to those cars I worked on back in the early 70’s. Unless you have extensive factor training on the car you are about to purchase, spend the money and get an extended warranty. There are many plans out there for your budget, but the best deal would be the 84 month and 100,000-mile plan. I have had these on 2 Grand Marquis’s, 1 F-150, 1 Mystique and now this 2014 Edge. It has paid for itself on all of those previous vehicles. If you lose a computer, a water pump, or a fuel pump in a PU truck, it will pay for itself right then and there. Everything that is going to happen to a car will happen the day after the factory warranty runs out!!!

How you gonna pay for it?

Only about 5% of the public can throw down $36,500 in cold hard cash to purchase a set of wheels outright. Ideally cash is king, but most of us will have to finance the majority of the purchase price. This is where you really need to do your homework before you ever set foot on a dealership lot!! And remember, dealership financing is your absolute last resort.

If you have a vehicle that you are going to either trade in or sell outright, then start here. Find out what your vehicle is actually worth. You might be surprised at how little that thing is worth. Used car values can be found on the web. Kelly Blue Book is one source, Edmunds and the NADA Guides are other good sources. These site will tell you what your vehicle is worth on a trade or to a private sale. In most cases, you will get more money for the vehicle from a private sale. But, the realization is – will you be able to sell it?

If your local area is saturated with that type of vehicle, you may have trouble trying to sell it, or getting the fair market value. In my case, I had a 2005 Ford F-150. It was basically a work truck. These things are all over the place on the road, and just about every used card dealer has 3 or 4 of them. If this is your case, trading it in might be the best option. In my case, the different would have been about $400.

Once you know about how much your vehicle is worth and how much cash you can put toward the purchase, now it is time to figure out your financing scheme. The best deal will be through a member owned credit union and the worst will normally be dealer financing or a loan clearing house such as Household Finance and Ge Capitol. Whomever you secure a deal though, the terms you are offered will be based on your calculated credit risk – your credit score.

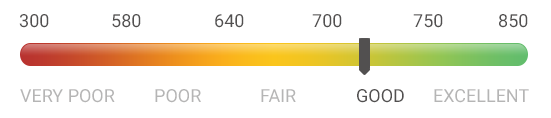

The FICO credit score is a three-digit number calculated from your credit report and is one factor used by lenders to determine your creditworthiness for a mortgage, loan or credit card. Your score can affect whether or not you are approved as well as what interest rate you are charged.

The magic number is around 700. If you have a score above that, you are considered a good risk for credit. If you score is under 600, then you are going to have problems securing a loan. The easiest way to get your credit score is to use a service such as Credit Karma. They offer a free service to show you your credit score from 2 of the 3 reporting agencies. You can get it from your home computer and there is a App for your phone or tablet. Not everything is free in life and neither is this. You will be subjected to a number of advertisements that deal with the financial industry. They also offer a number of other tools for helping secure your credit if you choose to use them.

The process of shopping for a loan can be a challenge, but if you want to get the best deal, then accept the challenge!! Start with your banking institution. If they do not have an online application process, then I’d find me a new bank or credit union to deal with! Of course, if your financial institution is local, then by all means, walk in and talk with their loan counselors. You want to get pre-approved for a loan. This process will let you know just how much money the bank is willing to give you, what interest rate, and how long you will have to pay it back. Remember, this is only a pre-approval process and you are under no obligation to enter into any agreement. When you fill out this application, you want to specify an amount slightly higher than what you are actually going to ask for. If you will need to borrow $25,000, then try to get pre-approved for $28,000. This will give you some leeway just in case there are some other expense in the car buying process that you did not account for.

The interest rate is how much extra money you are going to pay back to the lender on top of the money you borrowed. This is their profit or commission for lending you the money. In our example above, 48 months of payments at $475 equals a total payout of $22,800 on an original lending amount of $21,500. The lender is making $1,300 off this transaction at a rate of 2.9%. In today’s economy (2016), Interest rates are pretty low and you should be able to secure a deal for less than 3% if you have good credit.

If you are one of the 75% of Americans that have a credit score lower than 600, then you are going to find it difficult or impossible to find an interest rate lower than 3%. Shop around until you find the best deal. Give the dealer an opportunity to give you a quote, but when they ask you for the best deal you have so far, just smile and tell them to find you the best deal so you can compare rates on a competitive basis. Once you have a few quotes, then you can start playing once against the other. If these lenders are willing to loan you money, then they want your business and they might be willing to deal a few points here and there to secure your business.

Loaning money is a money making opportunity for those that have money to lend. A loan amortization schedule is setup such that approximately 75% of the interest will be paid down during the first 25% of the loan life cycle. The lender is going to get their money up front in the event you default on the deal! In our 4-year example, you are going to pay $975 out of the $1300 in interest during the first year of the loans life cycle. This is why loaning money is such a lucrative business!!

Now that you have selected the car to purchase, it is time to get with the financial institution and finish the paperwork and get the check. Remember that although you are pre-approved for a certain amount of money, the lender is only going to loan you an amount that is less than or equal to the fair market value of the car. Most lending institution that use the online application process, will allow you to type in a Vehicle Identification Number (VIN) and after answering a few other questions, will give you what they consider the fair market value of that vehicle which is also the maximum amount they will loan on that vehicle. If the amount you are going to finance is more that the fair market value of the car, then you will have to come up with the remainder.

The car buying process can be fun and enjoyable if you do your homework well in advance.

- You are here:

-

Home

- Blog